Thoughts on Braze (BRZE)

Tough times not over yet

Summary

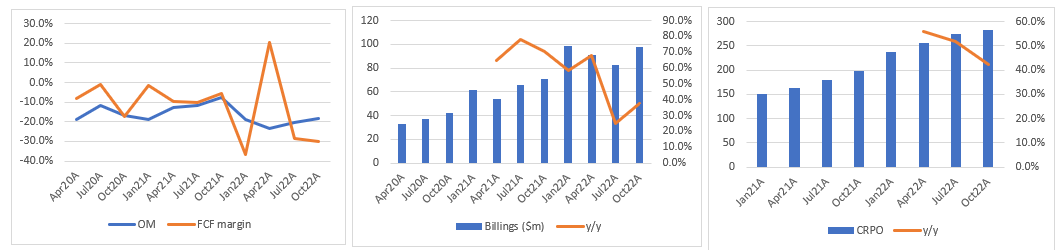

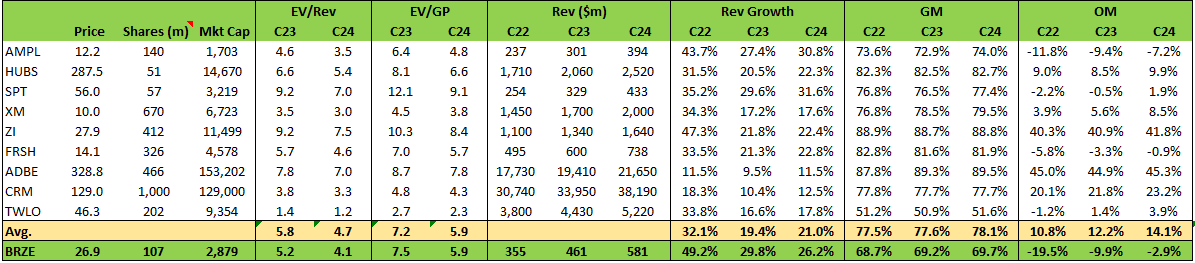

Despite the 65% YTD drawdown and significant underperformance vs IGV, I’d still have a short bias and see potential for another 20-25% downside for the stock. At 5.9x C24 EV/GP (on my numbers), Braze trades inline with its peer group. However, they won’t generate FCF until 2025 so there’s no real valuation support. The next catalyst isn’t until Q4 results in March.

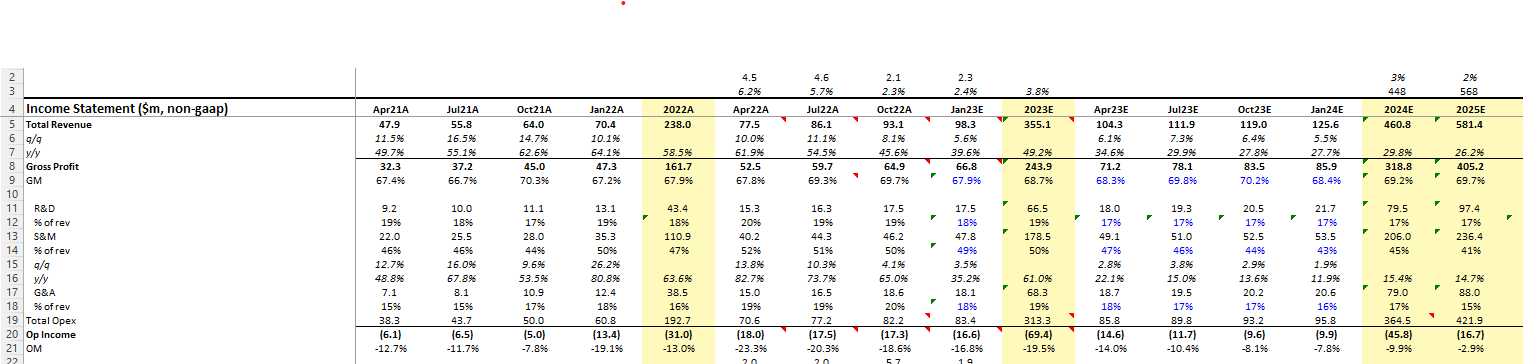

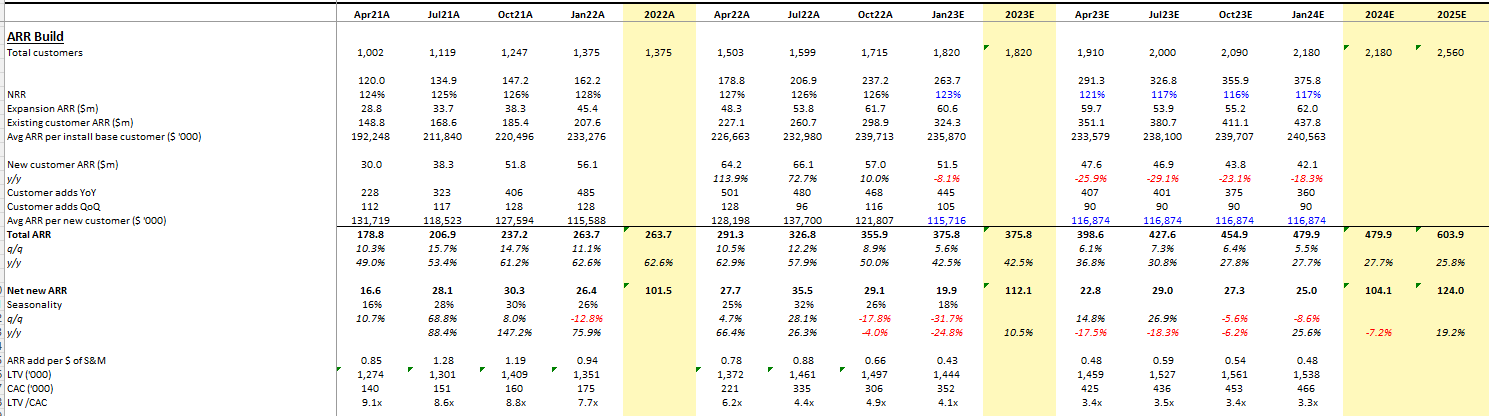

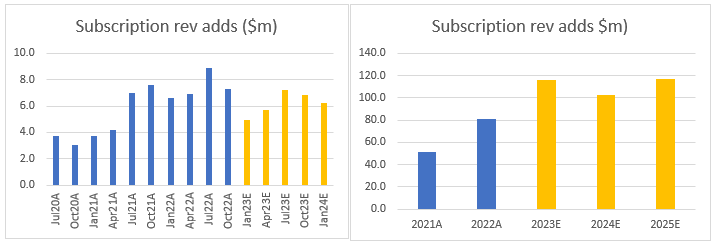

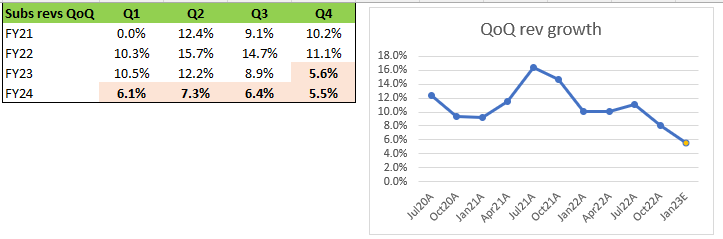

Braze was a clear covid beneficiary and Q2/Q3 results disproved the bull thesis that they would be less impacted by macro relative to marketing peers due to their focus on engagement over new customer acquisition. The key debate now is on 2023 growth. Management guided to ~3% sequential growth in Q4, raising the question if sub-30% growth is possible in 2023. My base case is 2023 revenue grows ~30% to $461m. The initial guide likely starts in the mid- to high-20s range to leave room for increases throughout the year. 30% growth implies net new ARR declines 7% yoy – the Q4 guide implies new ARR is down > 25% yoy.

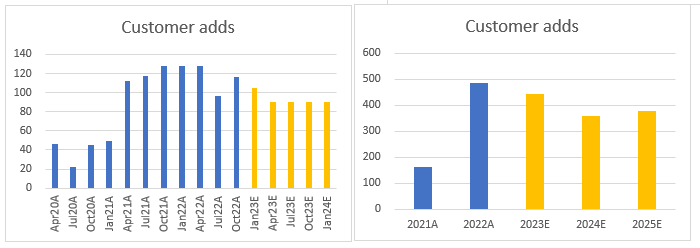

Net customer adds averaged less than 50 a quarter pre-covid and increased to a peak of 128 adds for three quarters in 2021/2022. The last two quarters have seen net adds decline vs peak levels, but the impact of macro/covid hangover is just beginning to be felt (imo). Braze has a ~6 month sales cycle for enterprise customers. Macro outlook began to deteriorate significantly starting in the second half of 2022 so the impact to new customer adds should really begin to be felt in Q4. Management said sales cycles have began to elongate, particularly for new business. The CEO has talked in the past about how Braze is typically additive to marketing/advertising budgets rather than direct replacement – this will also be a headwind to new business as budgets are pressured in 2023. Sales productivity has been an issue the last two quarters and the company has had to redesign their training program as a result. S&M spend is on pace to grow > 60% this year vs revenue growth of < 50%. Calculated unit economics and sales efficiency have begun to decline following the covid boost and it’s likely Braze has over-hired going into a slowdown.

NRR has declined from 128% to 126% (136% to 129% for > $500k ARR customers). NRR is calculated on a trailing twelve-month basis, so in periods when reported NRR is declining, the NRR in the most recent quarter is likely lower than reported NRR. The main driver of NRR is expansion in forward estimates of monthly active users (MAUs). It’s clear customers who signed contracts in 2021 are not expanding MAUs at the same rate in 2022. Q4 has the highest contract dollar value up for renewal for the full year and expansions should be particularly hard this quarter. Customers renewing in Q4 signed contracts in either late 2020 or late 2021 – periods when the forward outlook for Brazes key verticals was very strong.

So overall, Braze is facing headwinds to existing customer expansion due to MAU slowdown while new business is impacted by the greenfield nature of Braze’s solution in a period of tightening budgets. Operating margin will come in at around -20% this year and Braze won’t generate FCF until 2025. At 5.9x C24 EV/GP the stock still isn’t cheap and the lack of FCF means there’s no real valuation support. All this leads me to have a short bias for the stock, although I think the risk/reward on the short is better if the stock trades to the low-30s first.

Model & Charts

Feel free to send me an email or DM on Twitter if you’d like me to send the full model. I’m happy to share it.

Income statement

ARR build

Relevant charts

What does BRZE do?

Braze provides a cross-channel customer engagement platform that allows customers to design and execute marketing/engagement campaigns. Primary competition includes the legacy marketing clouds (CRM/ADBE and TWLO) along with a handful of private companies such as Airship, Iterable, Leanplum, and MoEngage.

Customers integrate Braze’s SDKs directly into their apps/websites. This enables real time ingestion of data into the Braze platform and allows Braze to send in-app messages. Braze claims their differentiation comes from the ability to orchestrate cross-channel campaigns (both in-product and out of product) and their platform is based on real-time data/insights as opposed to legacy marketing clouds that rely on batch processing.

In-product messaging channels include in-app pop ups and contact cards. Out of product channels include push notifications, email, SMS, and they announced WhatsApp would be added in 2023. For the out of product channels such as email/SMS, Braze only provides the orchestration layer and utilizes (and pays) other providers, such as Twilio, to deliver the messages. These costs show up in cost of sales and are part of the reason for Braze’s lower GM compared to peers. Q4 is typically the low point for GM each year due to the high volume of messages sent (Black Friday, Christmas, etc.).

To give an example of how the product works, imagine you’re on a hotel website looking to book a stay for New Years. You see there is availability and click “book now” to see the price. You’re directed to the check out page, but the price is more than you want to spend so you click back to browse the amenities page while you debate if the price is worth it. On the back end, you’ve just triggered an abandoned cart since you clicked book now, but subsequently left the page. The hotel has set up a rule using Braze that if a customer abandons a booking, but remains on the website, it triggers an in-app pop up prompting the customer to finish the booking. So while you’re looking at the amenities page you see a pop up that says something like “There’s only a few rooms left available for your selected date. Book now before it’s too late!” You exit out of the pop up and leave the website. The hotel knew this was a possibility, so they set up another rule in Braze saying if the pop up is ignored, follow up with an email reminder to the customer in 6 hours to come back to complete the booking. You get the email later that night and delete it. The hotel isn’t giving up and, using Braze again, they set up another rule that if the email doesn’t prompt the customer to complete the booking, send the customer a text message with a coupon code. You wake up in the morning to a text message from the hotel saying “Book by end of day and save 10% off your next stay!” You click the link in the text message and use the coupon to book the room you originally wanted at 10% off. This entire customer engagement journey was designed using the Braze platform.

Pricing structure

There has been lots of debate around Braze’s pricing structure and how the growth or decline in MAUs impacts contract pricing. I’ll try to do my best to explain the contract structure and the implications as I understand it.

Braze is a subscription company, but they do not price based on the number of seats. Contract values are determined by multiple factors:

1. Level of MAUs (~50% of total contract value)

2. Message volume (~30% of contract value)

3. Platform fee

4. Add-on features

Despite the MAU and message volume portion being somewhat usage/transaction based, Braze’s contracts are still recognized as revenue ratably over the contract length. Historically contracts have average length of 24 months and are paid annually in advance. In Q2/Q3 though, management has conceded that customers are opting for signing one-year contracts over two-year contracts and are paying semi-annually or quarterly rather than paying the full year upfront. This dynamic is impacting RPO and billings calculations and is also a headwind to FCF. Braze also bills mostly in USD (except for a portion in Yen) so FX hasn’t been a direct impact to the business, but the strong dollar has been a headwind to international customer expansion. > 40% of revenue comes from outside the US. Expenses are paid in local currency so the strong dollar has been a tailwind to margins.

Level of MAUs: Customers commit to an estimated level of MAUs for the upcoming year and Braze determines a price based on this number. If actual MAUs exceed the amount agreed on in the contract, customers pay overage fees or opt for an early renewal where the contract is extended and reset based on the higher MAU level. Overage fees have not been a meaningful portion of revenue in the past. If MAUs are below the agreed upon level, customers are still responsible for paying the full value of the contract, but (all else equal) they will downsize the contract at next renewal to reflect the lower MAU level.

MAU growth is important because it is the primary way customers grow their spend with BRZE. The CFO said the following on the Q1’23 earnings call – “So the monthly active user continues to be the single largest component of our top line, and we've been talking about that since actually before the IPO when we were talking to you guys in education sessions. The other components, CPM-based messaging, those are less than the MAU, but also growing fairly quickly. So the MAU will continue to be kind of a large component and will also drive additions to our dollar-based net retention.”

Message volume: The second largest portion of contract value comes from committed message volumes for email/SMS. The message volumes are use it or lose it and if customers go over pre-committed limits, they pay overage fees. As described above, Braze only provides the orchestration layer for emails/SMS and utilize third parties (like Twilio) to deliver the messages. Braze pays the email/SMS providers for this service and it shows up in cost of sales – this is one of the reasons for its lower GMs relative to the broader software group. Braze’s in-product messaging channels were developed internally and therefore are higher margin products. Management has talked about in the past that how they would pass on the business if a customer relies too heavily on SMS as an engagement method.

CEO on Q1’23 earnings call: “When we pursue business like SMS, we ensure that it fits the margin profile that we expect. And if it doesn't make sense in international market, we're not prioritizing that business. We know that the use cases that we run are ones that are high-value, high ROI as I go back to a lot, the sophistication of the platform is in the customer centricity of it, and that's where we're looking for our pricing power. So we're not chasing high-volume, low-margin business anywhere in the world.”

Platform fees and add-on features: These two make up the remaining portion of contract values, but I don’t think either of these are key for the near term results of the business. Customers pay a fee access the Braze platform and can opt for add on features such as Braze Currents that allows data to be exported in real time to partner systems.

Contract example: A hypothetical example is probably the best way to see how this contract structure is currently playing out for Braze. Say I’m a Braze customer that runs a quick-service restaurant that uses an app to manage orders and rewards program. My contract for BRZE has just come up for renewal. This past year, I had an average of 10,000 MAUs, which grew 20% yoy. This year I’m projecting 30% growth in average MAUs because I’ve opened more locations and expect increased adoption of the app. I share this growth projection with BRZE and sign a new contract for the upcoming year based on an estimated MAU level of 13,000 (10,000 x 30% estimated growth), even though my MAU level is only 10,000 today – remember contracts are priced based on forward estimates. My contract value increases to reflect increased MAU expectation.

Six months later, a global pandemic hits and all restaurants are forced to close indoor seating and all orders must be placed through an app for take-out. App usage skyrockets. MAUs are now growing 100% yoy vs my 30% prior expectation. Braze reaches out to say I’ve breached our contractual agreement for MAUs – my current MAU level is 20,000 (10,000 x 2) vs the 13,000 used in the contract. I have two choices: pay overage fees (which are expensive) or do an early renewal. I choose early renewal – BRZE is happy because I’m extending my contract for another year and I’m happy because I avoided expensive overage fees. However, business is going so well that I decided to sign a contract based on MAU growth of 125% for the next year vs current run rate of up 100% yoy. I do this because the super nice BRZE sales rep told me he’d give me a discount if I commit to 125% MAU growth now, but his boss won’t let him be so nice if I come back in 6 months and ask for another early renewal. I commit to the 125% MAU growth to lock in the “great price” and the sales rep goes home with his fat commission check. My contracted MAU value is now for 29,250 (13,000 MAU value in last contract x 2.25), while my run rate MAU is currently 26,000 (13,000 x 100% realized yoy growth).

Another year goes by and it’s time for another renewal. Turns out the pandemic didn’t last forever. Restaurants reopened and I’ve lost customers to competitors. My MAU growth for the year was only 80% vs the 125% projection in my contract. As I look forward to next year projections, I’ll be happy if I can keep MAUs flat and my current MAU level is 23,400 vs the last contracted level of 29,250. I tell my Braze rep that I’m expecting flat MAUs yoy and the dollar value of my contract based on MAUs declines to reflect this.

This example is obviously made up, but I think it’s reasonable to assume Braze is facing many conversations similar to this situation today. Think of all the covid beneficiaries – restaurants, ecommerce, digital health, etc. – this could apply to. The financial impact from this for should continue to be felt through the first half of 2023, because customers who signed in fiscal Q4’22 and Q1’23 likely projected much better MAUs than they have realized. I expect Q4 to be difficult due to this dynamic as management said Q4 has the highest dollar value of contracts up for renewal for the year.

Valuation

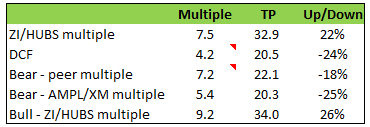

I generally view valuation as more of an art than science. For Braze, I used relative valuation and a simple DCF to frame potential outcomes for the stock. The conclusion is that I still think risk is skewed to the downside, but ideally would look for a price closer to low-30s before taking a short any meaningful size.

On a relative basis, ZI/HUBS are the two most relevant high-quality peers and they trade at a premium to BRZE. Assuming Braze traded at the average EV/GP (I use EV/GP for Braze given structurally lower GM relative to software group) multiple of these two on C24 numbers, the target price would be $32.9 (22% upside). Realistically, I don’t see any reason why the multiple should positively re-rate in the near term.

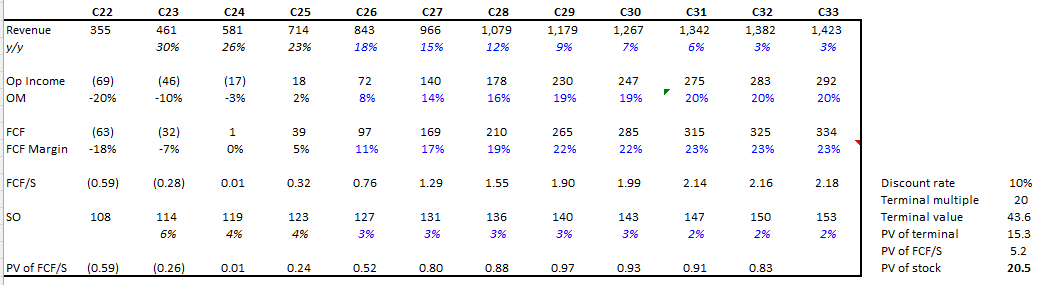

Using a 10-year simple DCF, the target price is $20.5 (24% downside). The DCF assumes revenue grows at a 15% CAGR to reach $1.4bn in C32 and operating margin reaches 20% - inline with long-term guidance from management. Share dilution starts at 6% (inline with 5-6% guide from management) and declines to 3% as growth slows. I then use a 20x terminal FCF multiple and 10% discount rate.

For a bear case, I assume net new ARR declines 20% in C23, which is less than the > 25% decline implied by the Q4 guide. Using the peer group EV/GP multiple (7.2x) on my bear case C23 GP, I get a target price of $22.1 (18% downside). If I use an average multiple of AMPL/XM (5.4x), two of the lower quality companies in the peer group, the target price is $20.3 (25% downside).

For a bull case, I assume net new ARR grows 20% yoy and use the average C23 EV/GP multiple of ZI/HUBS (9.2x). This results in a $34 target price (26% upside). For what it’s worth, I view this scenario as very unlikely. New business will be much harder to win in C23 and if we get a price closer to this $34 bull case, I would feel pretty comfortable putting on a decent short as the stock would be pricing in what I believe to be an unrealistic scenario.

Ownership

Braze has a dual class share structure, which is pretty standard for the 2020-2021 software IPO cohort. Per the most recent 10Q, Class B shares control 88% of the voting power. I generally don’t mind investing in companies that have this structure and frankly I prefer it sometimes. However, it does impact any potential acquisition because the insiders would need to agree to sell. I don’t think Braze is an acquisition target in the near term anyway. The most logical buyers would be someone like CRM/ADBE, but Braze purposely doesn’t integrate with CRM making them an unlikely buyer and ADBE just did a large acquisition.

VC/PE firms still own > 30% of the outstanding shares. Eventually these firms will sell down so from a tactical standpoint, I’d be concerned any strength in the stock could be met with selling pressure.

Relevant commentary from earnings recent calls

Macro

Q1’23

CEO: I'll wrap my remarks with a few comments on the state of the macro environment generally. While the world is confronting increased macroeconomic volatility and geopolitical uncertainty, we remain confident in our outlook. We had a great quarter and feel very good about our fiscal 2023 outlook. Our commitment to helping our customers build strong and lasting customer relationships through great customer engagement becomes even more relevant in a challenging environment. And we believe that our customers will continue to prioritize our services even in times of uncertainty.

CFO: So overall, I think we -- our continued outlook continues to be strong, and we're really excited about the rest of the year. Pipeline, geographically, remains diverse. It remains diverse across industries. And so what we've seen over the last several quarters is continued strength in kind of our top 5 verticals, continued growth in some of the smaller verticals, and we're kind of continuing to see that evolution. Geographically, we've had some folks travel over to Europe and get some face-to-face time with customers over there. Some of our leadership has gone over there, and they came back really enthusiastic.

Q2’23

CEO: However, the quarter was not without its challenges. Like many of our software peers, we saw elongated deal cycles and greater scrutiny on customer spend as some prospective and existing customers took a wait-and-see approach to the economy before committing to new investments. This effect was most acute as the quarter came to a close in July and affected our new customer ACV in the quarter. Notably, this period of rapid evolution in the sales environment overlapped with the ramp period for a large class of account executives hired earlier this year, resulting in sales productivity, landing short of where we expected it to be in the quarter. We are adapting quickly, identifying areas where execution faltered and making appropriate adjustments. In sales, we have returned to in-person training and mentorship while developing skills and presenting new tactics designed to help our account executives better navigate this dynamic environment. Specifically, we have launched new certification programs, engaged in more active competitive training, organized in-person sales boot camps for all new account executives and are regularly hosting in-person role playing, demo sessions and more. These are training opportunities that are far more available to us now that the world has largely reopened, and we are excited to be arming our salespeople with the knowledge required to further differentiate our offerings from those of both our legacy marketing cloud and startup competitors.

CEO: Despite the challenges we've recently encountered, we feel good about our pipeline, and new opportunity generation was strong in the quarter. Pipeline quality is a function of robust discovery and a strict qualification and inspection process. We continue to refine and improve our qualification criteria and are optimizing our middle-of-the-funnel nurture techniques.

CFO: So deferred revenue in the quarter, it's impacted by a few factors: how long we give our customers to pay; the extent to which we're able to actually bill on annual upfront terms; the contract start date relative to the signature date; and then, of course, the overall bookings that happened during the period. So during Q2, we saw greater demand for semiannual, quarterly payment terms. We saw more contracts with some delayed start dates. and then to a lesser extent, you have some requests for some additional time to pay. And so these factors taken together compounded the impact of some of the elongations of the sales cycles that you saw.

Q3’23

CEO: That said, we did continue to see some of the macroeconomic headwinds reported by many of our software peers, including elongated deal cycles and increased scrutiny on software investments, particularly with new business. In contrast, upsells were particularly strong, achieving a new high watermark in the quarter, led by success with our global strategic accounts.

CFO: As Bill remarked, our pipeline remains strong, and we continue to see solid demand for customer engagement solutions. However, like many of our peers, we continue to experience macroeconomic headwinds across geographies and industry verticals. These challenges manifest in elongated sales cycles, slower new business growth and fewer multiyear contracts. As such, we are continuing to approach our forecast prudently and guide on a risk-adjusted basis.

CEO: But one thing that we haven't seen as robust in Q2 and Q3 as we have through prior year periods are those people who signed a 12-month deal upfront, more of them are opting to continue on a 12-month deal just because of environment. But we expect much like we did through a lot of the jitters that were in the economy during COVID. It moved buyer sentiment toward those shorter contracts. And we saw a reversion of that and people got more comfortable with longer-term contracts once we got out of the depths of the COVID year in 2020. And so we're not overly concerned about that for the long-term health of any of these customer contracts, but you certainly see the impact on RPO.

NRR

Q2’23

CEO: And so there are certainly cases where certain clients don't hit their own internal growth targets. And so maybe they've purchased a monthly active user account for a year that upon renewal, they don't feel that they're going to achieve that anymore or there other situations where maybe they were planning on rolling out a new channel like e-mail or SMS and maybe they don't pace as far ahead. And so at renewal time, we look at rightsizing those allocations. I would say that historically, because of the continued expansion of the product, whenever we run into circumstances like that, there's also, in almost all of those cases, appetite for customers to continue to purchase new enhancements of the Braze product, whether those are looking at our data features around things like Currents or maybe our intelligence features, experimenting with the new channel like Content Cards or adding SMS or other things that we've continued to add to the bag of goods for our sales team to be out there selling. And so at renewal time, even in historical situations where there's been under consumption on one of those, the product footprint has been expanding so quickly that we've really been able to, in those situations, maintain or, in many cases, increase the size of those contracts with existing customers. We similarly have continued to achieve better pricing power over time as we continue to grow our awareness in the market and as we can point to the outsized ROI that the sophistication of a solution like Braze brings to our customers. And so those things all coming together have always been a -- an opportunity for us to continue to grow our customers, even when you potentially see things like a monthly active user account, prediction not being achieved or other similar circumstances like that.

CFO: So we don't guide on dollar-based net retention. So I would just -- the only thing I would say there is it is a 12-month trailing statistic. And so looking back historically, we do have some higher numbers that we'll be rolling off. And so we'll have to contend with that. So we don't guide on that, but just certainly take that into consideration.

Q3’23

CEO: And actually, through Q3, we had our lowest amount of available renewable dollars. But we saw those renewal conversations acting for -- across the whole year. We saw those renewal conversations acting pretty similarly to Q2, we're seeing it in Q4 as well. So a lot of the cross-sell and upsell motions that we're used to are still intact. I would say one of the things that we're seeing that's impacting the downside is that there are still -- there's a lot of turnover happening within teams as layoffs are happening in other parts of the economy, there's been a lot of M&A type disruption activity.

New customers

Q1’23

CEO: So we have a long track record of coming in and starting out with either replacing or consolidating other places. We also often are part of net new budgets, especially when there's new initiatives. So if you look at the kind of move toward direct-to-consumer type offerings that are happening in places like sports leagues or in media streaming, media and streaming, or even in like consumer packaged goods industries or with QSRs, like all of these are great examples where they've been building more direct-to-consumer digitally enabled offerings. And so those are part of net new budgets because they're brand-new corporate initiatives.

Q2’23

CEO: We're also obviously helping out -- helping on the services ecosystem side, which is that one of the blockers that often exists is just not having enough internal technical resources to go through implementations. Everything you've heard me talk about with respect to the GSIs and the marketing -- the large kind of marketing agency holding companies, that applies at the top end to be able to help those enterprises be able to move when maybe they wouldn't have been able to otherwise due to resourcing. But across the rest of the business looking all the way down into the SMB segment, we are also cultivating a huge community of smaller growth agencies and digital agencies all around the world that are able to come in and really help complement the strategy and advice that Braze provides directly with hands on keyboard and with more specific services that really help them get up and running more quickly and more comprehensively.

CEO: So we saw changes in some of the overall win rates that we track in pipeline because of just -- when we push things out, when I went back to that robust inspection and qualification process in our pipeline, we need to make sure that there are compelling date events and that there are -- there's a compelling reason for the business to make the change for us to spend our time on it. And so we certainly saw a few more of those as wait-and-see. If a wait-and-see kind of pushed out more than 3 months, we would prefer to close that out of the pipeline and then regenerate it once we have the compelling event coming back in. We also did see some pockets of customers choosing to go -- to stick with their existing providers or potentially go to much lighter weight solutions just because of some of the budget pressures that they're under. We've seen historical competitive situations like that, especially with – especially if we're in a vertical or an industry or a geography that happens to be more price sensitive. And what we've really noticed over time is that as those companies mature, as those geographies or those verticals continue to mature, that those customers come back. And when they do, they're ready to really pick a premium option, invest more in it, get more out of it. And so we did see some isolated instances of that in the quarter, but nothing that I think we haven't seen historically in other similar circumstances.

CFO: So they were -- so I think if we go back to -- Q4, I think, was sort of fairly back-end loaded more so than we had experienced historically. I would say Q1 and Q2 both were still more back-end loaded. We typically do about a little more than 50% of our business in the last month of the quarter. And within that last month, we'll do most of that at the very end of the month. I would say that was fairly characteristic of this quarter from a month-to-month perspective. In that last month, we did an overwhelming amount of the business at the very end of the month. And so that dynamic is also coming into play.

Margins

Q1’23

CEO: We really -- when we pursue business like SMS, we ensure that it fits the margin profile that we expect. And if it doesn't make sense in international market, we're not prioritizing that business. We know that the use cases that we run are ones that are high-value, high ROI as I go back to a lot, the sophistication of the platform is in the customer centricity of it, and that's where we're looking for our pricing power. So we're not chasing high-volume, low-margin business anywhere in the world. And so you should expect that to kind of continue to be our dynamic, as Isabelle just walked through.

Q2’23

CFO: At this time, we feel the investments we have made to date position us well to continue to drive sustainable growth while delivering on our commitment at our Analyst Day in October to focus on our path towards profitability. While headcount will continue to increase moderately as we close out FY '23 and look ahead into next year, we have recently chosen to slow our recruitment activity for net new hiring. Therefore, while this investment momentum will continue into the beginning of next year, you should expect the rate of OpEx growth to moderate as we increase our focus on driving operating leverage across the business.

Are you sure that the MAU part of the contract is only about 50% of ACV?